We saw some pretty unusual stuff on the markets last week. There is a lot of nervosity in the markets. A foretale of more significant moves?

The crazy stuff

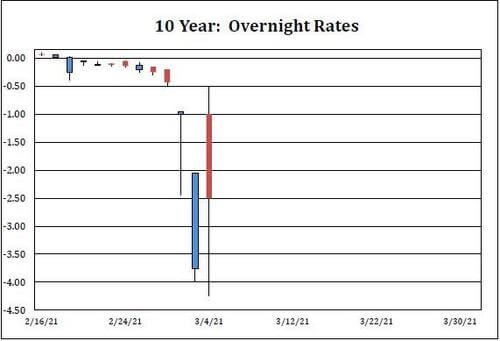

- The repo on the 10 Y treasury has reached 4.25% on Thursday, which is more than the failure to deliver rate. The demand for borrow was such that virtually all the bonds at the treasury fed ($14.5 bn) were on loan.

- Rates were on historical lows. When rate rally started, all the investors rushed to the door at the same time. It’s not over; analysts are forecasting a further increase in the yield.

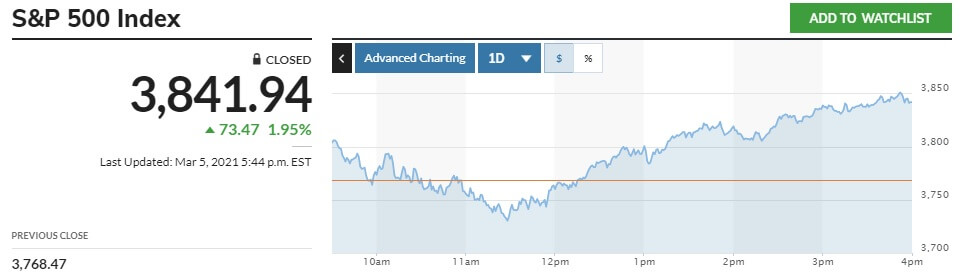

- On Friday, the S&P dropped ~2% from its opening, before closing up 1.95%. Those typed of behaviors are typical of a strong market nervosity (read “volatility”), even if it is not materialized yet in the close-to-close volatility calculations.

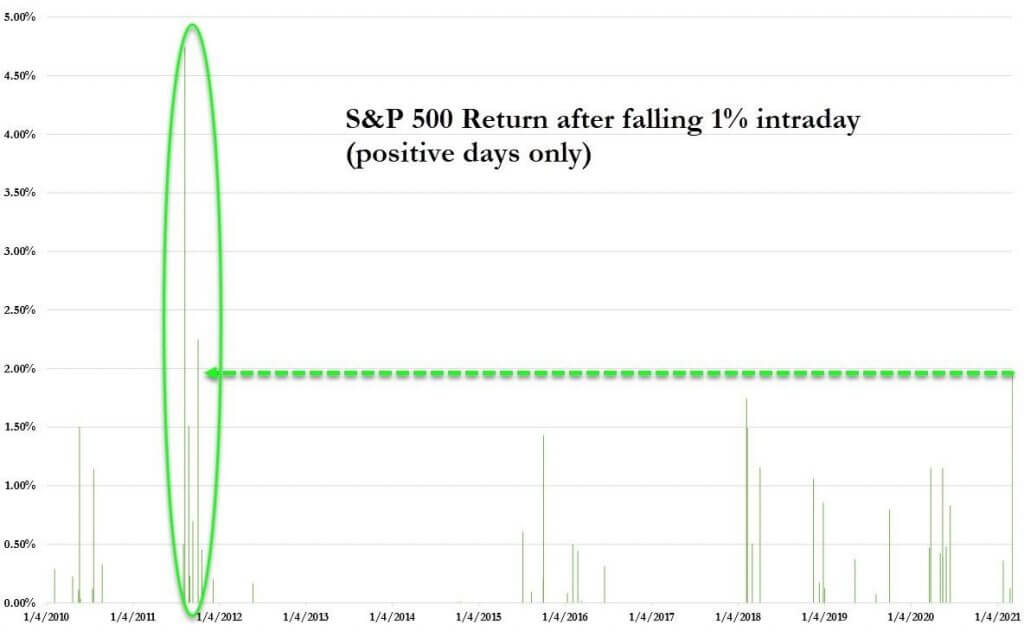

- On the S&P, Friday was one of the largest intra-day reversal ever:

- Actually, the VIX rallied up to 32 on Powell’s speech, before closing back at 24 on Friday

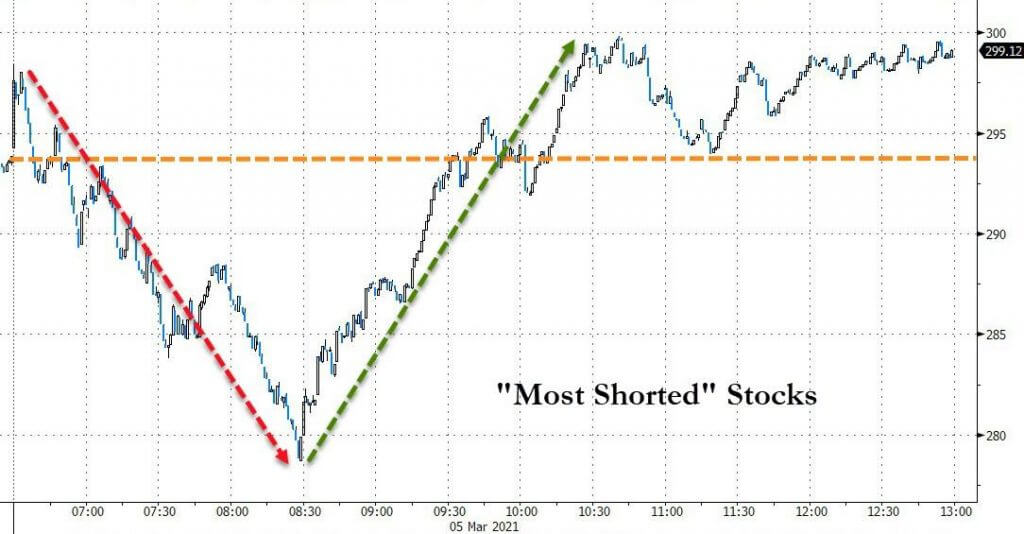

- There was a rotation of stocks in the S&P, with notably a rally of the most shorted stocks

Going forward…

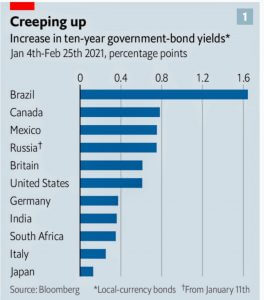

- The rates are not rising just in the US. It is a global issue

- The equity market is overvalued, but the Fed and the new 1.9 Tn stimulus plan supports the economy. The eternal question is – for how long? Could an event trigger a crash?

- Talking about a possible event, Nick Panigirtzoglou, JP Morgan’s quant analyst, 60:40 funds now have to rebalance and sell an estimated $107 Bn of equities. This will come on top of $110 bn of redemptions from pension investors, $22 Bn from Norges Bank, and $34 from Japan’s government pension fund, bringing the expected selling pressures on equities around $316 Bn for the end of this quarter.

Menu