‘When you combine ignorance and leverage, you get some pretty interesting results.” Warren Buffett

‘When you combine ignorance and leverage, you get some pretty interesting results.” Warren Buffett

Three good notes from the derivatives research teams of Morgan Stanley, Société Générale and Nomura point to a potential squeeze in the VIX, as a result of the increasing retail activism.

The Morgan Stanley paper

The Morgan Stanley paper states several interesting points:

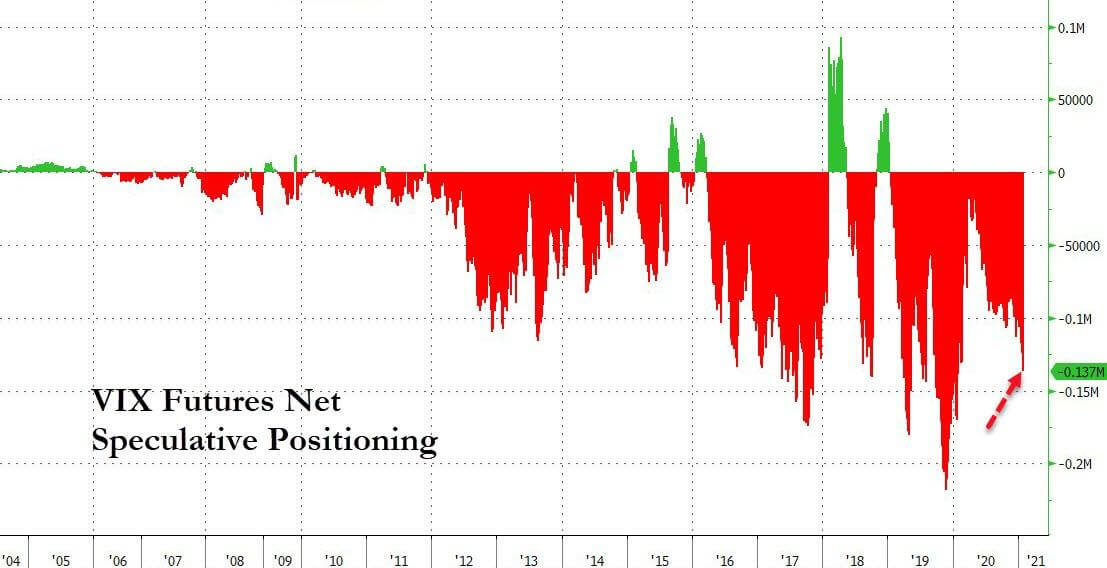

- VIX ETPs have seen a significant increase in inflows, resulting in a spike of 71k futures bought (~50% of ADV).

- A significant increase in open interest in the VIX ETP calls.

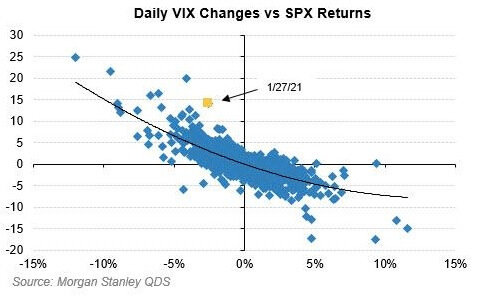

- On January 27th, VIX moved up by much more than its standard relation to the S&P indicates.

- The inflows to VIX ETPs generate risks which are usually taken on the short side by hedge funds, which are not exactly the friends of activists.

- Interestingly enough, retail traders are less prone to taking their gains, and therefore unlikely to sell when the VIX goes up, than professionals would, reducing the mean-reverting effect.

- And Morgan Stanley to conclude that indeed there is an increased risk of a volatility squeeze.

The Société Générale paper

Here are the main points from Société Générale:

- The equity short sellers included many long-short portfolio managers. If they had to deleverage their shorts, they also had to deleverage their longs. This impacted the companies usually bought by hedge funds in the tech segments.

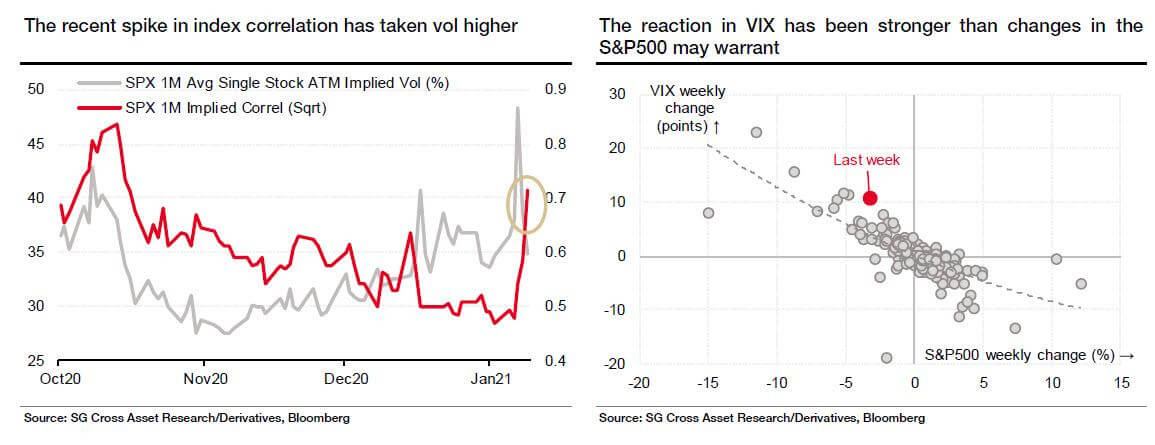

- The deleverage coincided with (caused?) a spike in market correlation. With the regular increase in single stock vols of the last few months, this has lead to an increase in the S&P vol and the VIX.

- Vol-controlled fund and momentum funds are at their maximum leverages, and will have to deleverage at some point, resulting in more downside pressure of the market.

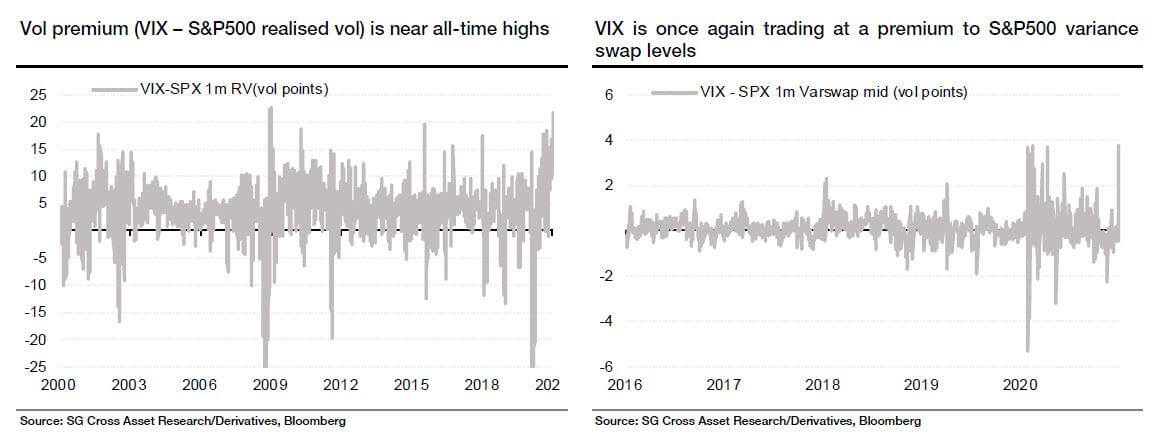

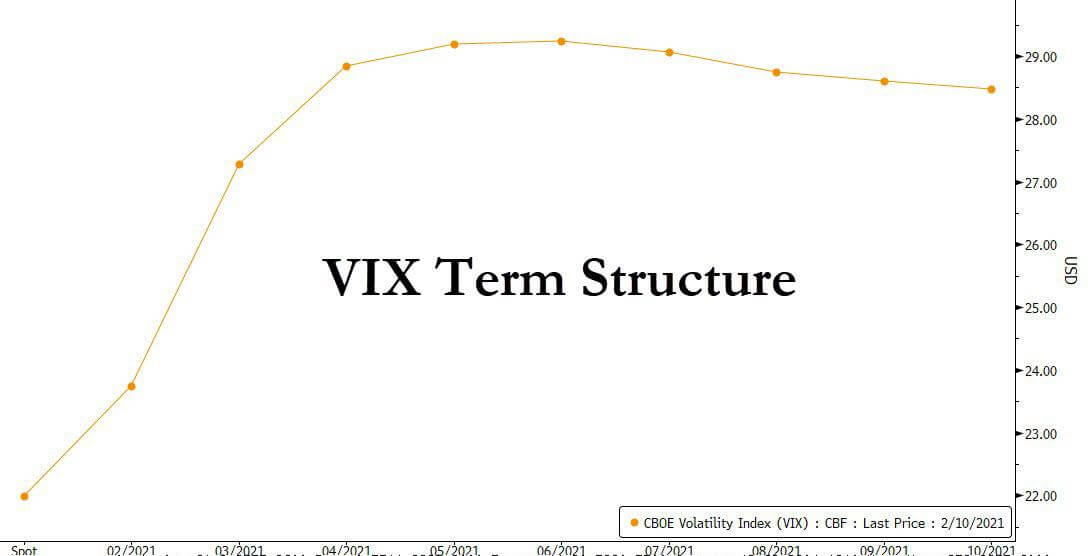

- VIX is now at a historic premium to historic vols and 1M varswaps, which has met low trading volumes recently. It would be a good moment to sell convexity.

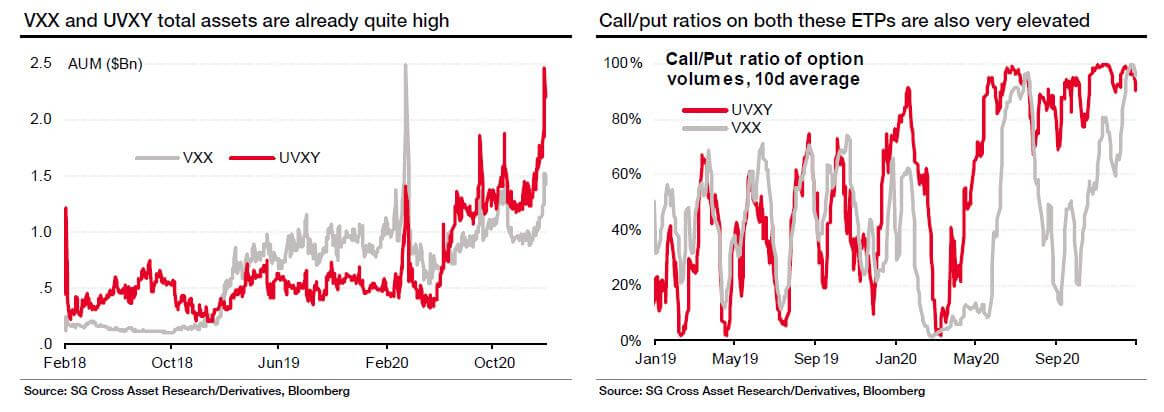

- That’s where SocGen’s idea that the Reddit crowd could take advantage of these elevated levels of VIX. If the GameStop traders carry their positions into VIX ETPs, we could see some large upward moves in vols/VIX. We are already at elevated AUM and Call demand:

- The WSB horde has a tendency to jump from one stock to another, and there is an increased chatter about volatility on those social media.

- Considering the weak open interest on VIX ETF options, and that there is a significant speculative short position on the VIX, a crowd moving onto their calls would have a significant impact on their levels.

- So the French bank is hinting at possible coming turbulence in the implied vol market, although it also warns that a repeat of the February 2018 Volmageddon is unlikely.

- Such a move up would be short-dated, since

- There is still more hidden liquidity in vol than in penny stocks.

- Volatility is structurally mean-reverting.

- VIX prices are bound by S&P options, a very liquid market.

- VIX options deleverage quickly as their own volatility rises, automatically reducing their leveraging benefit.

- A fall in S&P would not generate a VIX spike as high as February 2018, because the current vol levels are already much higher than in 2018.

- The French bank nevertheless recommend to move away from short term VIX shorts to more longer-dated bets like Dec21/Dec22 S&P forward variance or Dec21 Var-Vol spreads.

The Nomura paper

A third paper, by Nomura, indicates

- that the VIX spot went down last week, while the rest of the term structure remains well bid.

- While VIX increases are usually due to put buying, this time it seems that the purchase was mostly in S&P call purchases.

- Which means it is unlikely that the VIX will go any lower. The recent VIX decrease is probably just due to the higher vol-of-vol.

- The bigger risk right now is a spot-up, vol-up situation

- Meanwhile, the cause of the elevated long-term structure comes from regulators preventing firms from selling crash insurance through various stress-testing metrics, while ETN growth keeps supporting demand, notably a $42m vega purchase just last week, causing the first short-covering from the roll-down players.

- In other words, the situation is not about to get better, and the VIX market is indeed prone to a squeeze.

Jerome Powell back in 2012 admitted tacitly that “The Fed Has A Short Volatility Position.” If retail traders squeeze the VIX, they will go straight against the interest of the Fed…

Worse, their long VIX position would incentivize them into a market crash – exactly what the Fed is exactly trying to avoid… to protect retail investors!

Credits:

- Amanda Levenberg at Morgan Stanley

- Jitesh Kumar and Vincent Cassot at Société Générale

- Charlie McElligott at Nomura

Related articles:

Robinhood’s $65m SEC penalty and the ‘gamification’ of trading