An interesting article from Vineer Bhansali and Jeremie Holdom at LongTail Alpha offers a bi-modality interpretation of return expectations. The analysis offers some an interesting analysis of asset price forecasts implicit in option prices, as well as applications in asset allocation and portfolio construction.

An interesting article from Vineer Bhansali and Jeremie Holdom at LongTail Alpha offers a bi-modality interpretation of return expectations. The analysis offers some an interesting analysis of asset price forecasts implicit in option prices, as well as applications in asset allocation and portfolio construction.

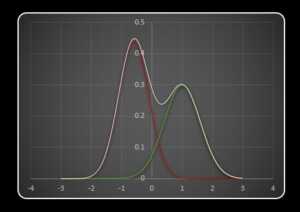

A stock price is the average of all possible future outcome, where ‘average’ is guided by a probability distribution which can be measured from option prices. We usually assume that there is one such lognormal distribution of returns. The authors assume that there is two lognormal distributions, which both have their own expectation and volatility, and whose relative weights can change over time. The distribution with a higher expectation is ‘optimistic’ in nature, while the other represents a ‘pessimistic’ view of the world.

Numerical outcomes and their interpretations

The numerical results are surprising:

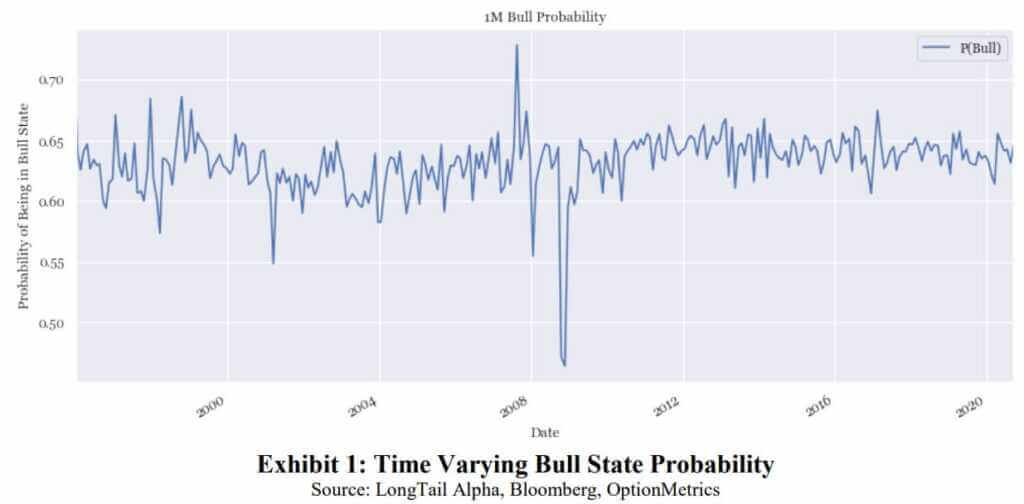

- 1 month S&P volatilities over the last 25 years of data indicate that, to a few exceptions, the relative weight of the two modes is stable, with ~63% weight to the ‘optimists’:

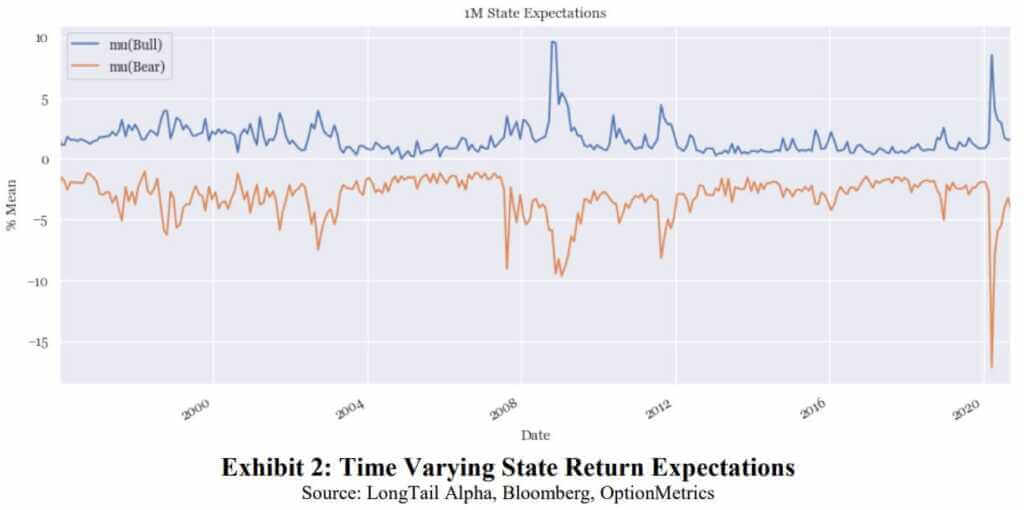

- On the other hand, return expectations are less stable.

- Expectations diverge in times of crisis – the bears become really bear:

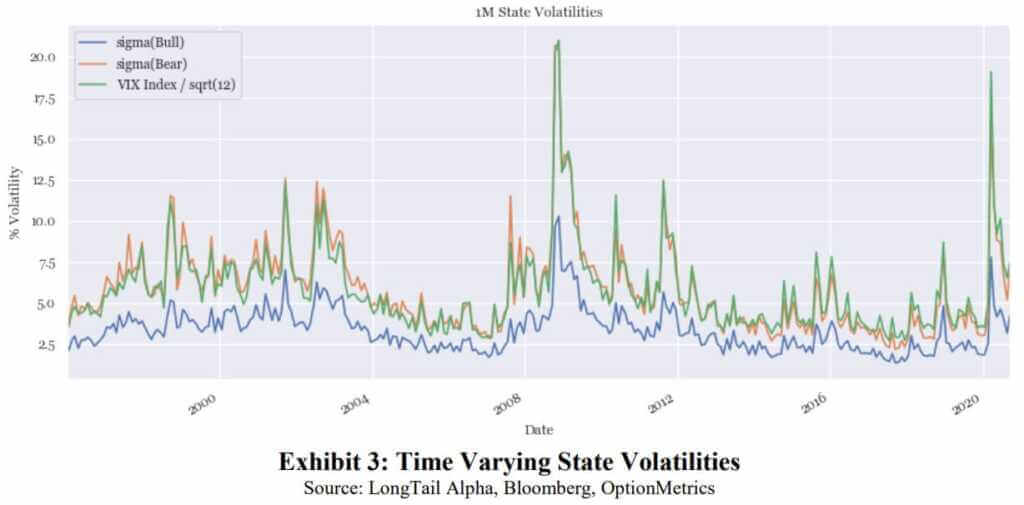

- The volatilities of these two distributions are in synch.

- The volatility of the bearish view is higher than the optimistic viewpoint.

- Th bearish volatility is also surprisingly close to the VIX, which confirms that the ‘fear gauge’ directionally is a good representation of ‘crash risk’:

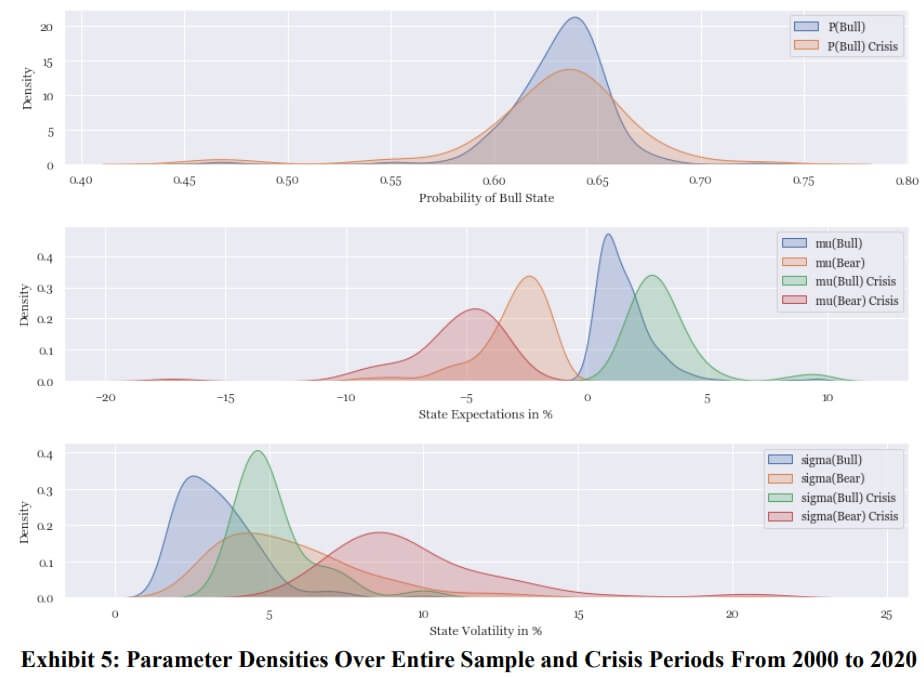

- The model’s 5 degrees of liberty (relative weight, the two expectations μ and the two volatilities σ) each have their own distribution probabilities. Splitting time-wise over ‘quiet’ and ‘crisis’ periods (VIX>25), we get the densities below.

- In crisis times, expectations and volatilities are typically double their ‘quiet’ values.

- The relative weight fattens in crisis times, indicating that there is more uncertainty in which mode the market will evolve, but that the long-term vision of the world remains optimistic.

- The bear distribution of volatilities is constantly wider than for the bulls – there is much more uncertainty in hell than in heaven.

- The fat right tails indicate that hell can really become unpleasant.

- In quiet times, it would be a good idea to buy reinsurance, which will become extremely expensive in crisis due to forced liquidations and lack of sellers:

Application to portfolio construction

The authors are pointing to several consequences in the portfolio construction phase:

- By construction, the unimodal and the bimodal representations have the same overall expectancy and volatility. The two world views differ essentially by their skew – the bimodal interpretation is much more skewed to the left.

- A classical mean-variance optimization considering bi-modal assets would not pick that skew, as the approach takes only the first two moments in consideration. But a utility function taking large moves into consideration (say, with a term quadratic in returns) will be sensitive to the skew. By introducing a lower skew (aka more downside risk), bimodality will reduce the allocation to the asset.

- The relative weight of the two modes seems stable at 63%. Unfortunately, the first two overall moments of the S&P are very sensitive to this relative weight parameter. Should it be imprecisely measured, the overall expectation and the overall volatility change significantly, and an asset allocation would be significantly impacted. A simple portfolio (S&P + cash) would instantly move into cash or into S&P if we move the relative mode weight by 10% or 15%.

- The authors are suggesting adding puts or calls in the universe to counterbalance this last effect. Well, maybe.

Conclusion

This bimodal interpretation will certainly lead to volatility surface arbitrage strategies, or at least to a better understanding of skew and asset pricing developments. There are also many further analysis to develop in asset allocation. Beforehand, the model should certainly be verified on other instruments.

References

Good piece though. Here are the references:

- Good States, Bad States: What Do Options Tell Us About Schizophrenic Behavior of Mr. Market and What Can We Do About It?

- https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3737144